Hey there! Are you a student struggling to refinance your student loans due to a low credit score? Don’t worry, there are still options available for you. With the rising cost of education, many students are facing the burden of student loan debt. In this article, we will explore some options for student loan refinance even if you have a low credit score. Let’s find a solution that works for you!

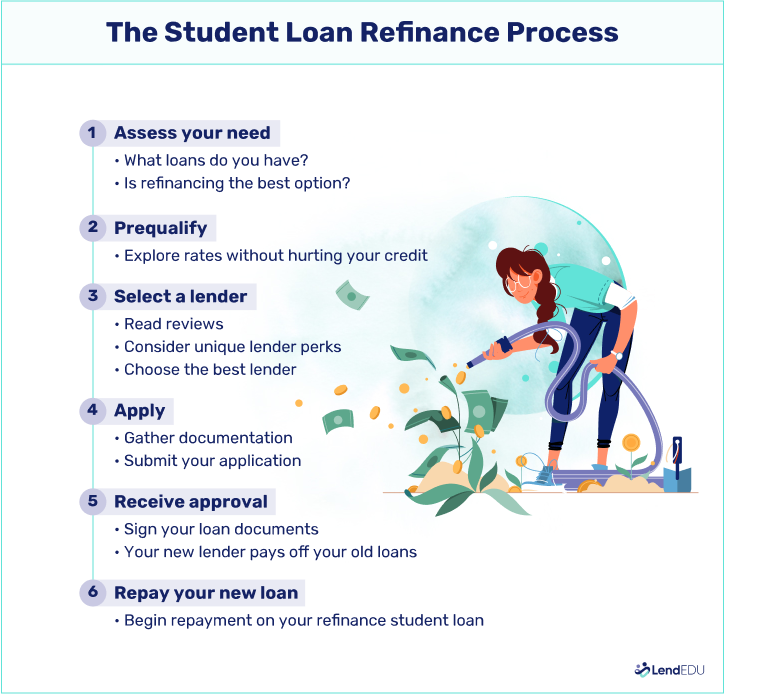

Importance of Student Loan Refinance

Student loan refinance can be a game-changer for individuals who are struggling to make their monthly payments. With the burden of student loan debt weighing heavily on many recent graduates, finding a way to lower monthly payments can provide much-needed relief. Refinancing allows borrowers to combine multiple student loans into one new loan with a potentially lower interest rate, saving them money in the long run. This can result in lower monthly payments, making it easier for borrowers to stay on top of their debt and avoid falling behind.

Additionally, student loan refinance can help borrowers improve their financial situation in the long term. By securing a lower interest rate, borrowers can save thousands of dollars over the life of their loan. This can free up funds that can be put towards other financial goals, such as building an emergency fund, saving for a down payment on a house, or investing for the future. Refinancing can also help borrowers pay off their loans faster, as they can choose a shorter repayment term and save on interest charges.

Another key benefit of student loan refinance is the potential to improve credit scores. By consolidating multiple loans into one new loan, borrowers can simplify their repayment process and make it easier to stay on track with their payments. Making consistent, on-time payments on a refinanced loan can help borrowers build a positive credit history and improve their credit score over time. This can open up opportunities for better financial products and lower interest rates in the future.

For borrowers with a low credit score, student loan refinance can be a lifeline. While traditional lenders may be hesitant to work with individuals with a low credit score, there are lenders who specialize in working with borrowers in this situation. These lenders may offer refinancing options specifically designed for individuals with less-than-perfect credit, allowing them to take advantage of the benefits of refinancing even with a low credit score.

In conclusion, student loan refinance can be a valuable tool for borrowers looking to improve their financial situation. By consolidating multiple loans into one new loan with a lower interest rate, borrowers can save money, pay off their loans faster, and improve their credit score. For individuals with a low credit score, refinancing can provide much-needed relief and help them get back on track with their finances. If you are struggling to keep up with your student loan payments, consider exploring the option of student loan refinance to see if it could benefit you.

Factors Affecting Credit Score

When it comes to student loan refinance with a low credit score, it is important to understand the factors that can affect your credit score. Your credit score is a numerical representation of your creditworthiness, and it is used by lenders to determine whether or not to approve your loan application. Here are some key factors that can impact your credit score:

Payment History: One of the most important factors that affect your credit score is your payment history. Missing payments or making late payments can have a negative impact on your credit score, so it is crucial to make all of your loan payments on time.

Utilization Rate: Another factor that can affect your credit score is your credit utilization rate. This is the amount of credit you are using compared to the amount of credit you have available. Keeping your credit utilization rate low can help improve your credit score.

Length of Credit History: The length of your credit history is also an important factor in determining your credit score. Lenders like to see a long and positive credit history, so it is beneficial to keep old accounts open and maintain a good payment history.

Credit Mix: Having a mix of different types of credit, such as credit cards, student loans, and a mortgage, can also impact your credit score. Lenders like to see that you can manage different types of credit responsibly.

New Credit Inquiries: Every time you apply for a new loan or credit card, a credit inquiry is made on your credit report. Having too many new credit inquiries can have a negative impact on your credit score, so it is best to limit the number of new credit applications you make.

Public Records: Negative items such as bankruptcies, foreclosures, or liens can significantly impact your credit score. It is important to avoid these types of public records in order to maintain a good credit score.

By understanding these factors that can affect your credit score, you can take steps to improve your score and increase your chances of qualifying for student loan refinance even with a low credit score. Making on-time payments, keeping your credit utilization low, maintaining a positive credit history, diversifying your credit mix, limiting new credit inquiries, and avoiding negative public records can all help improve your credit score over time.

Strategies to Improve Credit Score for Refinancing

Having a low credit score can make it challenging to refinance your student loans at a lower interest rate. However, there are several strategies you can implement to improve your credit score in order to qualify for a lower interest rate when refinancing.

1. Make Timely Payments: One of the most important factors influencing your credit score is your payment history. Be sure to make timely payments on all of your debts, including student loans, credit cards, and any other outstanding balances. Set up automatic payments or reminders to ensure you never miss a due date.

2. Decrease Credit Utilization: Another factor that affects your credit score is the amount of credit you are using compared to the amount available to you. This is known as credit utilization. Try to keep your credit utilization below 30% to improve your credit score. You can achieve this by paying down existing balances or requesting a credit limit increase.

3. Diversify Your Credit Mix: Lenders like to see a diverse mix of credit types on your credit report, including installment loans (like student loans) and revolving credit (like credit cards). If you primarily have one type of credit, consider diversifying by taking out a small personal loan or getting a new credit card. Just be sure to use these new credit lines responsibly to avoid harming your credit score.

4. Resolve Errors on Your Credit Report: Mistakes on your credit report can significantly impact your credit score. Regularly review your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) to check for any inaccuracies. If you find errors, dispute them with the credit bureau to have them corrected.

5. Avoid Opening New Credit Accounts: While diversifying your credit mix can be beneficial, opening too many new credit accounts in a short period of time can actually harm your credit score. Each new credit inquiry can result in a small decrease in your score. Be strategic about when and how often you apply for new credit.

By implementing these strategies, you can gradually improve your credit score and increase your chances of qualifying for student loan refinancing at a lower interest rate. Remember that improving your credit score takes time, so be patient and consistent with your efforts. With dedication and responsible financial habits, you can achieve a higher credit score and secure better loan terms in the future.

Options for Students with Low Credit Score

Having a low credit score can make it challenging to refinance student loans, but there are still options available for students in this situation. Here are some possible solutions for students with low credit scores:

1. Co-signer: One option for students with a low credit score is to have a co-signer on their loan. A co-signer with a higher credit score can help students qualify for a lower interest rate and better loan terms. It’s important to choose a co-signer who has a good credit history and is willing to take on the responsibility of the loan if the student is unable to make payments.

2. Income-based repayment: Another option for students with low credit scores is to consider income-based repayment plans. These plans calculate monthly payments based on the borrower’s income, making it easier for students with lower credit scores to manage their student loan payments. While income-based repayment plans may not lower the overall cost of the loan, they can provide some relief for students struggling to make payments.

3. Explore lenders that consider other factors: Some lenders consider factors other than credit score when evaluating loan applications. Students with low credit scores may have better luck with these lenders, especially if they have a steady income or a strong co-signer. It’s worth researching different lenders to see if there are any that take a more holistic approach to evaluating loan applications.

4. Improve your credit score: While this option may take time, improving your credit score can help you qualify for better loan terms in the future. Students with low credit scores can work on improving their credit by making on-time payments, reducing debt, and monitoring their credit report for any errors. It’s also helpful to keep credit card balances low and avoid opening new lines of credit. By taking steps to improve your credit score, you can increase your chances of qualifying for student loan refinancing with better terms and lower interest rates.

Benefits of Refinancing Student Loans

Refinancing your student loans can have many benefits, especially if you have a low credit score. Here are five key advantages of refinancing your student loans:

1. Lower Interest Rates: When you refinance your student loans, you may be able to secure a lower interest rate than what you currently have. This can save you money in the long run by reducing the amount of interest you pay over the life of the loan.

2. Lower Monthly Payments: By refinancing your student loans, you can potentially lower your monthly payments, making it easier to manage your finances. This can be especially helpful if you are struggling to make ends meet due to a low credit score.

3. Combine Multiple Loans: If you have multiple student loans with different interest rates, refinancing can allow you to consolidate them into one loan with a single monthly payment. This can simplify your finances and make it easier to keep track of your payments.

4. Improve Credit Score: Refinancing your student loans can also help improve your credit score. By consolidating your loans and making consistent payments, you can demonstrate financial responsibility to creditors, which can boost your credit score over time.

5. Access to Better Repayment Options: When you refinance your student loans, you may have access to more flexible repayment options, such as income-based repayment plans or extended repayment terms. This can give you more control over your finances and make it easier to manage your student loan debt.

Overall, refinancing your student loans can provide a number of benefits, even if you have a low credit score. By taking advantage of lower interest rates, lower monthly payments, and improved credit scores, you can better manage your student loan debt and work towards financial stability. Consider exploring refinancing options to see how it can help you achieve your financial goals.

Originally posted 2025-08-31 10:00:00.